These 3 Countries Tried Socialism. Here’s What Happened.

Socialists are fond of saying that socialism has never failed because it has never been tried.

But in truth, socialism has failed in every country in which it has been tried, from the Soviet Union beginning a century ago to three modern countries that tried but ultimately rejected socialism—Israel, India, and the United Kingdom.

While there were major political differences between the totalitarian rule of the Soviets and the democratic politics of Israel, India, and the U.K., all three of the latter countries adhered to socialist principles, nationalizing their major industries and placing economic decision-making in the hands of the government.

The Soviet failure has been well documented by historians. In 1985, General Secretary Mikhail Gorbachev took command of a bankrupt disintegrating empire.

After 70 years of Marxism, Soviet farms were unable to feed the people, factories failed to meet their quotas, people lined up for blocks in Moscow and other cities to buy bread and other necessities, and a war in Afghanistan dragged on with no end in sight of the body bags of young Soviet soldiers.

The economies of the Communist nations behind the Iron Curtain were similarly enfeebled because they functioned in large measure as colonies of the Soviet Union.

In these trying times, we must turn to the greatest document in the history of the world to promise freedom and opportunity to its citizens for guidance. Find out more now >>

With no incentives to compete or modernize, the industrial sector of Eastern and Central Europe became a monument to bureaucratic inefficiency and waste, a “museum of the early industrial age.” As The New York Times pointed out at the time, Singapore, an Asian city-state of only 2 million people, exported 20% more machinery to the West in 1987 than all of Eastern Europe.

And yet, socialism still beguiled leading intellectuals and politicians of the West. They could not resist its siren song, of a world without strife because it was a world without private property. They were convinced that a bureaucracy could make more-informed decisions about the welfare of a people than the people themselves could. They believed, with John Maynard Keynes, that “the state is wise and the market is stupid.”

Israel, India, and the United Kingdom all adopted socialism as an economic model following World War II. The preamble to India’s constitution, for example, begins, “We, the People of India, having solemnly resolved to constitute India into a Sovereign Socialist Secular Democratic Republic … ” The original settlers of Israel were East European Jews of the left who sought and built a socialist society. As soon as the guns of World War II fell silent, Britain’s Labour Party nationalized every major industry and acceded to every socialist demand of the unions.

At first, socialism seemed to work in these vastly dissimilar countries. For the first two decades of its existence, Israel’s economy grew at an annual rate of more than 10%, leading many to term Israel an “economic miracle.” The average gross domestic product growth rate of India from its founding in 1947 into the 1970s was 3.5%, placing India among the more prosperous developing nations. GDP growth in Great Britain averaged 3% from 1950 to 1965, along with a 40% rise in average real wages, enabling Britain to become one of the world’s more affluent countries.

But the government planners were unable to keep pace with increasing population and overseas competition. After decades of ever-declining economic growth and ever-rising unemployment, all three countries abandoned socialism and turned toward capitalism and the free market.

The resulting prosperity in Israel, India, and the U.K. vindicated free-marketers who had predicted that socialism would inevitably fail to deliver the goods. As British Prime Minister Margaret Thatcher observed, “the problem with socialism is that you eventually run out of other people’s money.”

1. Israel

Israel is unique, the only nation where socialism was successful—for a while. The original settlers, according to Israeli professor Avi Kay, “sought to create an economy in which market forces were controlled for the benefit of the whole society.”

Driven by a desire to leave behind their history as victims of penury and prejudice, they sought an egalitarian, labor-oriented socialist society. The initial, homogeneous population of less than 1 million drew up centralized plans to convert the desert into green pastures and build efficient state-run companies.

Most early settlers, American Enterprise Institute scholar Joseph Light pointed out, worked either on collective farms called kibbutzim or in state-guaranteed jobs.

The kibbutzim were small farming communities in which people did chores in exchange for food and money to live on and pay their bills. There was no private property, people ate in common, and children under 18 lived together and not with their parents. Any money earned on the outside was given to the kibbutz.

A key player in the socialization of Israel was the Histadrut, the General Federation of Labor, subscribers to the socialist dogma that capital exploits labor and that the only way to prevent such “robbery” is to grant control of the means of production to the state.

As it proceeded to unionize almost all workers, the Histadrut gained control of nearly every economic and social sector, including the kibbutzim, housing, transportation, banks, social welfare, health care, and education. The federation’s political instrument was the Labor party, which effectively ruled Israel from the founding of Israel in 1948 until 1973 and the Yom Kippur War. In the early years, few asked whether any limits should be placed on the role of government.

Israel’s economic performance seemed to confirm Keynes’ judgment. Real GDP growth from 1955 to 1975 was an astounding 12.6%, putting Israel among the fastest-growing economies in the world, with one of the lowest income differentials. However, this rapid growth was accompanied by rising levels of private consumption and, over time, increasing income inequality.

There was an increasing demand for economic reform to free the economy from the government’s centralized decision-making. In 1961, supporters of economic liberalization formed the Liberal party — the first political movement committed to a market economy.

The Israeli “economic miracle” evaporated in 1965 when the country suffered its first major recession. Economic growth halted and unemployment rose threefold from 1965 to 1967. Before the government could attempt corrective action, the Six-Day War erupted, altering Israel’s economic and political map.

Paradoxically, the war brought short-lived prosperity to Israel, owing to increased military spending and a major influx of workers from new territories. But government-led economic growth was accompanied by accelerating inflation, reaching an annual rate of 17% from 1971 to 1973.

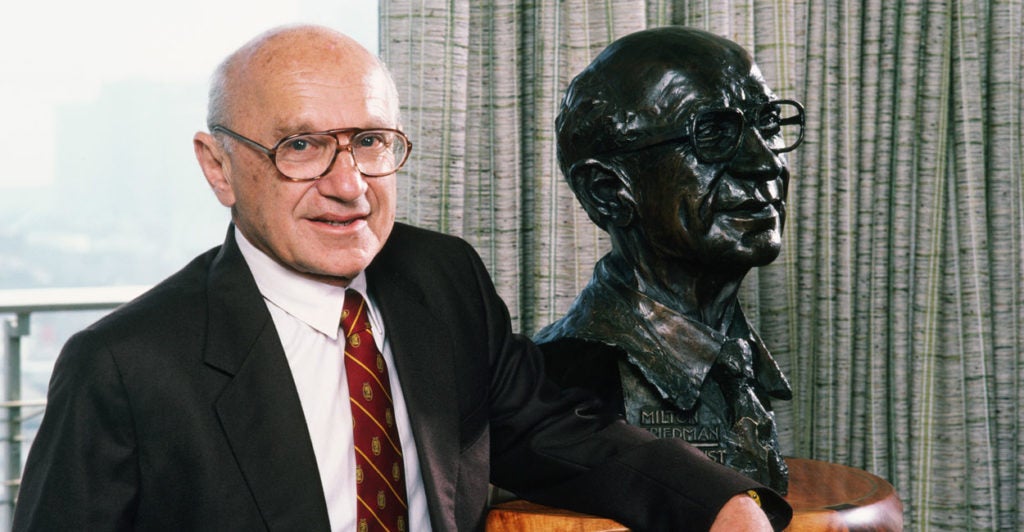

For the first time, there was a public debate between supporters of free-enterprise economics and supporters of traditional socialist arrangements. Leading the way for the free market was the future Nobel Prize winner Milton Friedman, who urged Israeli policymakers to “set your people free” and liberalize the economy.

The 1973 war and its economic impacts reinforced the feelings of many Israelis that the Labor party’s socialist model could not handle the country’s growing economic challenges. The 1977 elections resulted in the victory of the Likud party, with its staunch pro-free-market philosophy. The Likud took as one of its coalition partners the Liberal party.

Because socialism’s roots in Israel were so deep, real reform proceeded slowly. Friedman was asked to draw up a program that would move Israel from socialism toward a free-market economy. His major reforms included fewer government programs and reduced government spending; less government intervention in fiscal, trade, and labor policies; income tax cuts; and privatization. A great debate ensued between government officials seeking reform and special interests that preferred the status quo.

Meanwhile, the government kept borrowing and spending and driving up inflation, which averaged 77% for 1978-79 and reached a peak of 450% in 1984–85. The government’s share of the economy grew to 76%, while fiscal deficits and national debt skyrocketed. The government printed money through loans from the Bank of Israel, which contributed to the inflation by churning out money.

Finally, in January 1983, the bubble burst, and thousands of private citizens and businesses as well as government-run enterprises faced bankruptcy. Israel was close to collapse.

At this critical moment, a sympathetic U.S. president, Ronald Reagan, and his secretary of state, George Shultz, came to the rescue. They offered a grant of $1.5 billion if the Israeli government agreed to abandon its socialist rulebook and adopt some form of U.S.-style capitalism, using American-trained professionals.

The Histadrut strongly resisted, unwilling to give up their decades-old power and to concede that socialism was responsible for Israel’s economic troubles. However, the people had had enough of soaring inflation and nonexistent growth and rejected the Histadrut’s policy of resistance. Still, the Israeli government hesitated, unwilling to spend political capital on economic reform.

An exasperated Shultz informed Israel that if it did not begin freeing up the economy, the U.S. would freeze “all monetary transfers” to the country. The threat worked. The Israeli government officially adopted most of the free-market “recommendations.”

The impact of a basic shift in Israeli economic policy was immediate and pervasive. Within a year, inflation tumbled from 450% to just 20%, a budget deficit of 15% of GDP shrank to zero, the Histadrut’s economic and business empire disappeared along with its political domination, and the Israeli economy was opened to imports.

Of particular importance was the Israeli high-tech revolution, which led to a 600% increase in investment in Israel, transforming the country into a major player in the high-tech world.

There were troubling side effects such as social gaps, poverty, and concerns about social justice, but the socialist rhetoric and ideology, according to Glenn Frankel, The Washington Post’s correspondent in Israel, “has been permanently retired.”

The socialist Labor party endorsed privatization and the divestment of many publicly held companies that had become corrupted by featherbedding, rigid work rules, phony bookkeeping, favoritism, and incompetent managers.

After modest expansion in the 1990s, Israel’s economic growth topped the charts in the developing world in the 2000s, propelled by low inflation and a reduction in the size of government. Unemployment was still too high and taxes took up 40% of GDP, much of it caused by the need for a large military.

However, political parties are agreed that there is no turning back to the economic policies of the early years—the debate is about the rate of further market reform. “The world’s most successful experiment in socialism,” Light wrote, “appears to have resolutely embraced capitalism.”

2. India

Acceptance of socialism was strong in India long before independence, spurred by widespread resentment against British colonialism and the land-owning princely class (the zamindars) and by the efforts of the Communist Party of India, established in 1921.

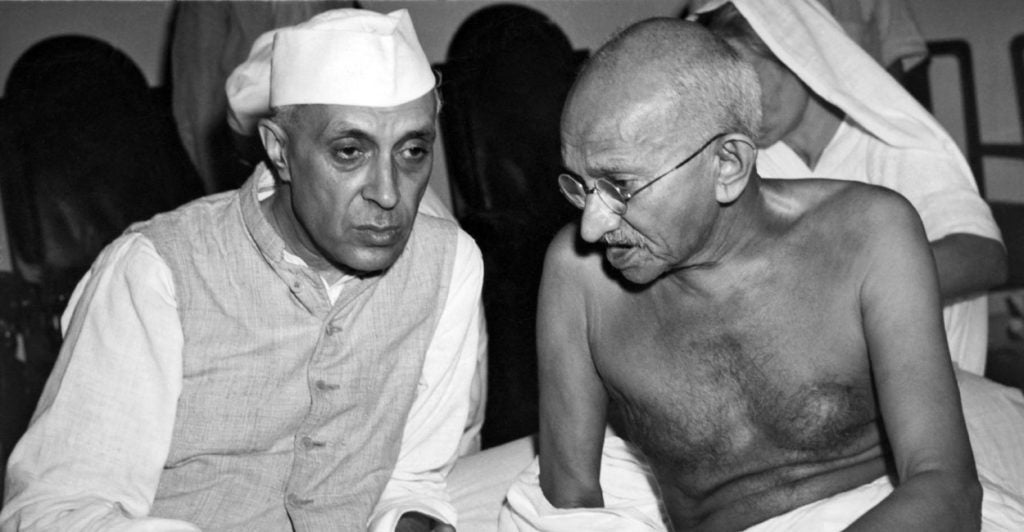

Jawaharlal Nehru adopted socialism as the ruling ideology when he became India’s first prime minister after independence in 1947.

For nearly 30 years, the Indian government adhered to a socialist line, restricting imports, prohibiting foreign direct investment, protecting small companies from competition from large corporations, and maintaining price controls on a wide variety of industries including steel, cement, fertilizers, petroleum, and pharmaceuticals. Any producer who exceeded their licensed capacity faced possible imprisonment.

As the Indian economist Swaminathan S. Anklesaria Aiyar wrote, “India was perhaps the only country in the world where improving productivity … was a crime.” It was a strict application of the socialist principle that the market cannot be trusted to produce good economic or social outcomes. Economic inequality was regulated through taxes—the top personal income tax rate hit a stifling 97.75%.

Some 14 public banks were nationalized in 1969; six more banks were taken over by the government in 1980. Driven by the principle of “self-reliance,” almost anything that could be produced domestically could not be imported regardless of the cost. It was the “zenith” of Indian socialism, which still failed to satisfy the basic needs of an ever-expanding population. In 1977-78, more than half of India was living below the poverty line.

At the same time, notes Indian-American economist Arvind Panagariya, a series of external shocks shook the country, including a war with Pakistan in 1965, which came on the heels of a war with China in 1962; another war with Pakistan in 1971; consecutive droughts in 1971-72 and 1972-73, and the oil price crisis of October 1973, which contributed to a 40% deterioration in India’s foreign trade.

Economic performance from 1965 to 1981 was worse than than at any other time of the post-independence period. As in Israel, economic reform became an imperative. Prime Minister Indira Gandhi had pushed her policy agenda as far to the left as possible.

In 1980, the Congress party won a two-thirds majority in the Parliament, and Gandhi adopted, at last, a more pragmatic, non-ideological course. But as with everything else in India, economic reform proceeded slowly.

An industrial-policy statement continued the piecemeal retreat from socialism that had begun in 1975, allowing companies to expand their capacity, encouraging investment in a wide variety of industries, and introducing private-sector participation in telecommunications.

Further liberalization received a major boost under Rajiv Gandhi, who succeeded his mother in 1984 following her assassination. As a result, GDP growth reached an encouraging 5.5%.

Economics continued to trump ideology under Rajiv Gandhi, who was free of the socialist baggage carried by an earlier generation. His successor, P. V. Narasimha Rao, put an end to licensing except in selected sectors and opened the door to much wider foreign investment. Finance minister Manmohan Singh cut the tariff rates from an astronomical 355% to 65%.

According to Arvind Panagariya, “the government had introduced enough liberalizing measures to set the economy on the course to sustaining approximately 6 percent growth on a long-term basis.” In fact, India’s GDP growth reached a peak of over 9% in 2005-08, followed by a dip to just under 7% in 2017-18.

A major development of the economic reforms was the remarkable expansion of India’s middle class. The Economist estimates there are 78 million Indians in the middle-middle and upper-middle-class category.

By including the lower-middle class, Indian economists Krishnan and Hatekar figure that India’s new middle class grew from 304.2 million in 2004-05 to an amazing 606.3 million in 2011-12, almost one-half of the entire Indian population. The daily income of the three middle classes are lower middle, $2-$4; middle middle, $4-$6; upper middle, $6-$10.

While this is extremely low by U.S. standards, a dollar goes a long way in India, where the annual per capita income is approximately $6,500. If only half of the lower-middle class makes the transition to upper-class or middle income, that would mean an Indian middle class of about 350 million Indians—a mid-point between The Economist and Krishnan and Hatekar estimates.

Such an enormous middle class confirms the judgment of The Heritage Foundation, in its Index of Economic Freedom, that India is developing into an “open-market economy.”

In 2017, India overtook Germany to become the fourth-largest auto market in the world, and it is expected to displace Japan in 2020. That same year, India overtook the U.S. in smartphone sales to become the second-largest smartphone market in the world.

Usually described as an agricultural country, India is today 31% urbanized. With an annual GDP of $8.7 trillion, India ranks fifth in the world, behind the United States, China, Japan, and Great Britain. Never before in recorded history, Indian economist Gurcharan Das has noted, have so many people risen so quickly.

All this has been accomplished because the political leaders of India sought and adopted a better economic system—free enterprise—after some four decades of fitful progress and unequal prosperity under socialism.

3. United Kingdom

Widely described as “the sick man of Europe” after three decades of socialism, the United Kingdom underwent an economic revolution in the 1970s and 1980s because of one remarkable person—Prime Minister Margaret Thatcher. Some skeptics doubted that she could pull it off—the U.K. was then a mere shadow of its once prosperous free-market self.

The government owned the largest manufacturing firms in such industries as autos and steel. The top individual tax rates were 83% on “earned income” and a crushing 98% on income from capital. Much of the housing was government-owned.

For decades, the U.K. had grown more slowly than economies on the continent. Great Britain was no longer “great” and seemed headed for the economic dust bin.

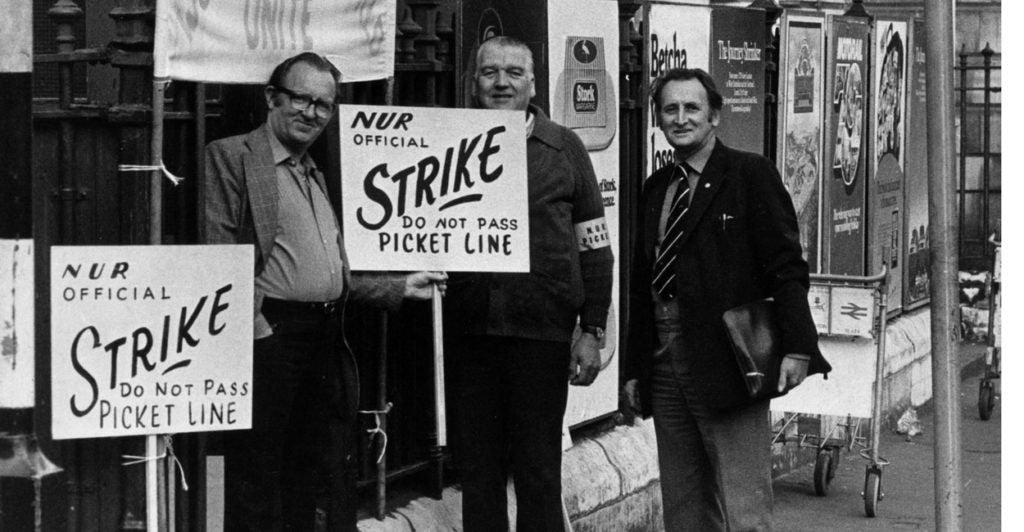

The major hindrance to economic reform was the powerful trade unions, which since 1913 had been allowed to spend union funds on political objectives, such as controlling the Labour Party. Unions inhibited productivity and discouraged investment.

From 1950 to 1975, the U.K.’s investment and productivity record was the worst of any major industrial country. Trade union demands increased the size of the public sector and public expenditures to 59% of GDP. Wage and benefits demands by organized labor led to continual strikes that paralyzed transportation and production.

In 1978, Labour Prime Minister James Callaghan decided that, rather than hold an election, he would “soldier on” to the following spring. It was a fatal mistake. His government encountered the legendary “winter of discontent” in the first months of 1979. Public-sector workers went on strike for weeks. Mountains of uncollected rubbish piled high in cities. Bodies remained unburied and rats ran in the streets.

Newly elected Conservative Prime Minister Margaret Thatcher, the United Kingdom’s first female PM, took on what she considered her main opponent—the unions.

Flying pickets, the ground troops of industrial conflict who would travel to support workers on strike at another site, were banned and could no longer blockade factories or ports. Strike ballots were made compulsory. The closed shop, which forced workers to join a union to get a job, was outlawed. Union membership plummeted from a peak of 12 million in the late 1970s to half that by the late 1980s.

“It’s now or never for [our] economic policies,” Thatcher declared, “let’s stick to our guns.”

The top rate of personal income tax was cut in half, to 45%, and exchange controls were abolished.

Privatization was a core Thatcher reform. Not only was it fundamental to the improvement of the economy, it was “one of the central means of reversing the corrosive and corrupting effects of socialism,” she wrote in her memoirs.

Through privatization that leads to the widest possible ownership by members of the public, “the state’s power is reduced and the power of the people enhanced.” Privatization “is at the center of any programme of reclaiming territory for freedom.”

She was as good as her word, selling off government-owned airlines, airports, utilities, and phone, steel, and oil companies.

In the 1980s, Britain’s economy grew faster than that of any other European economy except Spain. U.K. business investment grew faster than in any other country except Japan. Productivity grew faster than in any other industrial economy.

Some 3.3 million new jobs were created between March 1983 and March 1990. Inflation fell from a high of 27% in 1975 to 2.5% in 1986. From 1981 to 1989, under a Conservative government, real GDP growth averaged 3.2%.

By the time Thatcher left government, the state-owned sector of industry had been reduced by some 60%. As she recounted in her memoirs, about 1 in 4 Britons owned shares in the market. Over 600,000 jobs had passed from the public to the private sector. The U.K. had “set a worldwide trend in privatization in countries as different as Czechoslovakia and New Zealand.”

Turning decisively away from Keynesian management, the once sick man of Europe now bloomed with robust economic health. No succeeding British government, Labour or Conservative, has tried to renationalize what Margaret Thatcher denationalized.

The Lesson of China

How then to explain the impressive economic success of a fourth major economy, China, with annual GDP growth of 8 to 10% from the 1980s almost to the present?

From 1949 to 1976, under Mao Zedong, China was an economic basket case, owing to Mao’s personal mismanagement of the economy. In his avid pursuit of Soviet-style socialism, Mao brought about the Great Leap Forward of 1958-60, which resulted in the deaths of at least 30 million and perhaps as many as 50 million Chinese, and the Cultural Revolution of 1966-76, in which an additional 3 million to 5 million died. Mao left China backward and deeply divided.

Mao’s successor, Deng Xiaoping, turned China in a different direction, seeking to create a mixed economy in which capitalism and socialism would coexist with the Communist Party monitoring and constantly adjusting the proper mix. For the past four decades, China has been the economic marvel of the world for the following reasons:

It began its economic ascent almost from ground zero because of Mao’s ideological stubbornness. It has engaged in the calculated theft of intellectual property, especially from the U.S., for decades. It has taken full advantage of globalism and its membership in the World Trade Organization, while ignoring the prescribed rules against such practices as intellectual property theft. It has used tariffs and other protectionist measures to gain trade advantages with the U.S. and other competitors.

It created a middle class of some 300 million people, who enjoy a decent living and at the same time constitute a sizable domestic market for goods and services. It continues to use the forced labor of the laogai to make cheap consumer goods that are sold in Walmart and other Western stores. It allows an enormous black market to exist because Party members profit from its sales.

It permits foreign investors to buy into Chinese companies, but the government—i.e., the Communist Party—always retains a majority interest. It operates an estimated 150,000 state-owned enterprises that guarantee jobs for tens of millions of Chinese. It depends on the energy and experience of the most entrepreneurial people in the world, second only to Americans.

In short, the People’s Republic of China was an economic failure for its first three decades under Mao and Soviet socialism. It began its climb to become the second-largest economy in the world when it abandoned socialism in the late 70s and initiated its experiment, which so far has been successful, in capitalism with Chinese characteristics.

There are clear signs that such success is no longer automatic. China is experiencing a slowing economy, is ruled by a dictatorial but divided Communist Party clinging to power, faces widespread public demands for the guarantee of fundamental human rights, and suffers from a seriously degraded environment.

History suggests that these problems can best be solved by a democratic government ruled by the people, not a one-party authoritarian state that resorts to violence in a crisis, as Beijing did at Tiananmen Square and is doing in Hong Kong.

Socialism’s Fatal Conceit

As we have seen from our examination of Israel, India, and the United Kingdom, the economic system that works best for the greatest number is not socialism with its central controls, utopian promises, and OPM (other people’s money), but the free-market system with its emphasis on competition and entrepreneurship. All three countries tried socialism for decades, and all three finally rejected it for the simplest of reasons—it doesn’t work.

Socialism is guilty of a fatal conceit: It believes its system can make better decisions for the people than they can for themselves. It is the end product of a 19th-century prophet whose prophecies (such as the inevitable disappearance of the middle class) have been proven wrong time and again.

According to the World Bank, more than 1 billion people have lifted themselves out of poverty in the past 25 years, “one of the greatest human achievements of our time.” Of those billion, approximately 731 million are Chinese, and 168 million Indians.

The main driver of this uplift from poverty has been the globalization of the international trading system. China owes most of its success to the trade freedom offered by the U.S. and the rest of the world.

The latest edition of Index of Economic Freedom from The Heritage Foundation confirms the global trend toward economic freedom: Economies rated “free” or “mostly free” enjoy incomes that are more than five times higher than the incomes of “repressed economies” such as those of North Korea, Venezuela, and Cuba.

Israel’s socialist miracle turned out to be a mirage, India discarded socialist ideology and chose a more market-oriented path, and the United Kingdom set an example for the rest of the world with its emphasis on privatization and deregulation.

Whether we are talking about the actions of an agricultural country of 1.3 billion, or the nation that sparked the industrial revolution, or a small Middle Eastern country populated by some of the smartest people in the world, capitalism tops socialism every time.

Originally published by National Review.

No comments:

Post a Comment